Debunking Inflation Myths: The Truth Behind Tariffs, Trade, and Price Dynamics

Uncover the truth behind inflation myths in this post that demystifies how tariffs and trade are wrongly blamed for rising prices. Explore why an excessive money supply is the real driver of inflation, and learn to navigate the economic forces shaping investment strategies. Stay informed!

Inflation Unmasked: Learning from the Past to Navigate the Future

Inflation may seem like a complex economic beast, but at its heart lies a simple truth: when there’s too much money chasing too few goods, prices inevitably rise. In this post, we’ll unravel the mystery behind inflation by learning from historical missteps and debunking common myths, all while simplifying complex ideas into relatable concepts that can inspire your investment decisions.

The Core of Inflation: A Simple Equation

Imagine if everyone suddenly had twice as much money. With no additional goods available, people would bid higher for the same items, and prices would soar. This is the essence of economist Milton Friedman’s famous insight: "Inflation is always and everywhere a monetary phenomenon." In other words, when the supply of money in an economy grows faster than the production of goods and services, inflation is the natural outcome.

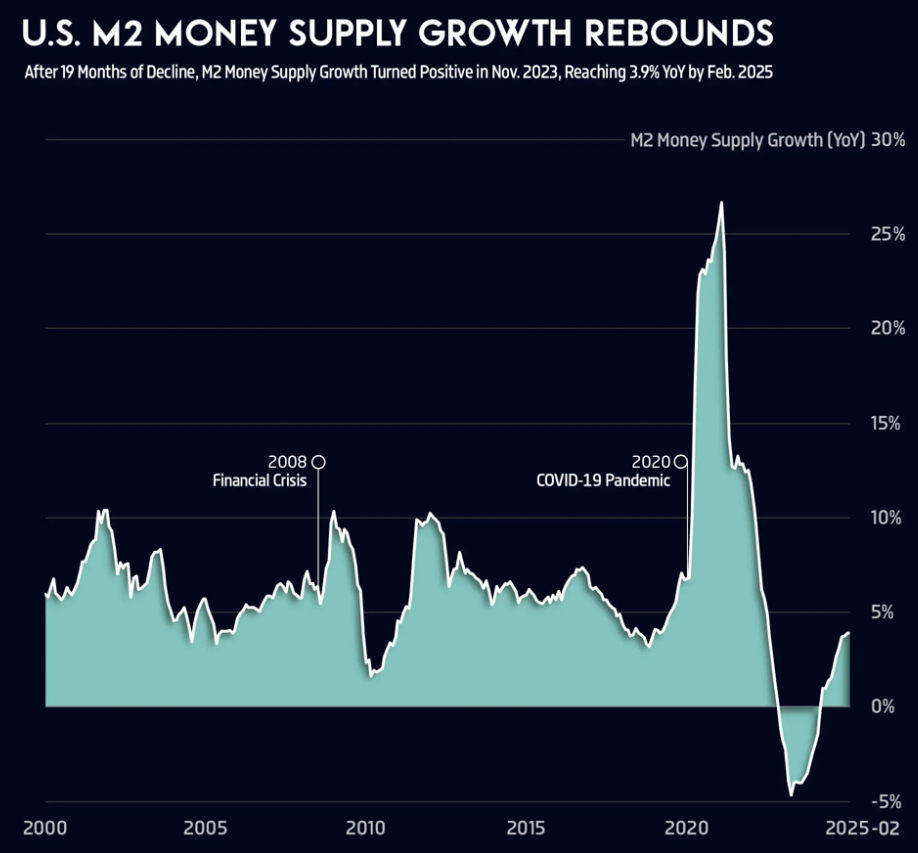

Central banks, such as the U.S. Federal Reserve, carefully monitor and control the money supply using tools like interest rates and quantitative easing. They use measures like the M2 aggregate, a sum of cash, checking deposits, and savings, to gauge the flow of money. When M2 grows too rapidly relative to the economy’s output, inflation tends to follow. This simple, yet powerful, relationship has shaped monetary policy for decades.

Debunking Inflation Myths: Separating Fact from Fiction

It’s easy to fall for sensational explanations when prices rise, but history teaches us to look deeper:

- Myth 1: Government Spending Alone Causes Inflation

Government expenditures only lead to inflation when financed by creating new money. Spending from taxes or borrowing doesn’t add new dollars into circulation. It’s when central banks “print” money to buy government bonds that inflation risks soar. - Myth 2: Tariffs and Trade Wars Trigger Broad Inflation

While tariffs might increase the cost of some goods, they usually just shift spending rather than elevate the overall price level. The real culprit is still an excessive money supply relative to available goods. - Myth 3: Supply Shocks Permanently Spike Prices

Natural disasters or shipping delays can cause temporary price hikes, but unless they are accompanied by an increase in the overall money supply, these shocks merely rearrange spending rather than sustain broad inflation.

In each case, the underlying theme is clear: the balance between money and goods is what truly drives inflation.

The Time Lag: When Money Takes Time to Change Prices

Changes in the money supply do not instantaneously alter price levels. Think of it as water filling a pipe, the faucet (money creation) may open fully, but it takes time for the pressure (prices) to build. After central banks inject money into the system, it might take months or even years for inflation to fully materialize. This delayed effect was vividly demonstrated during the COVID-19 pandemic, when unprecedented monetary easing eventually led to a significant inflation surge, only to be tempered later by aggressive tightening measures.

Why a Little Inflation is Not Always a Bad Thing

Central banks around the world have embraced a target of roughly 2% inflation. This modest rate is not a failure of economic control but a strategic choice to:

- Avoid Deflation: A slight inflation buffer helps prevent the damaging effects of falling prices, which can stall economic activity and deepen recessions.

- Anchor Expectations: When businesses and consumers expect 2% inflation, they can plan better for the future, leading to a more stable economic environment.

- Maintain Monetary Flexibility: Moderate inflation allows central banks room to cut interest rates during downturns, preventing scenarios like Japan’s prolonged near-zero interest environment.

- Manage Debt: With gradual inflation, the real burden of debt diminishes over time, making it easier for governments and borrowers to manage obligations.

In essence, a steady, predictable inflation rate of around 2% provides a balanced environment, one that encourages growth, stabilizes expectations, and prevents the economic pitfalls of deflation.

Lessons from History: Contrasting Crises

Two historical episodes, The Great Depression and the COVID-19 pandemic, offer stark lessons:

- The Great Depression (1930s): A drastic contraction in the money supply led to severe deflation. With banks failing and credit drying up, prices dropped, wages fell, and the economy spiraled downward.

- The COVID-19 Pandemic (2020s): To stave off a deflationary collapse, central banks injected massive amounts of money into the system. Although this flood of money eventually sparked high inflation, it also prevented an economic free-fall. The subsequent monetary tightening helped restore stability over time.

These contrasting cases underscore the importance of maintaining a careful balance. Too little money can choke an economy, while too much can overheat it. The key is to learn from past errors and adjust policies to foster sustainable growth.

Navigating Investments in an Inflationary World

For investors, understanding inflation isn’t just academic, it’s a roadmap for making smarter financial decisions:

- Real vs. Nominal Returns: Recognize that nominal gains can be misleading. If your portfolio earns 5% while inflation is 3%, your real growth is only 2%. Aim for returns that exceed inflation to truly build wealth.

- Diversification as a Shield: Different asset classes react uniquely to inflation. Equities can often pass on increased costs, real estate can yield rising rents, and inflation-protected bonds adjust with the CPI. A diversified portfolio balances these dynamics, reducing risk.

- Watch Central Bank Signals: The Federal Reserve’s actions on interest rates and money supply are like a weather forecast for the economy. Monitoring these signals helps anticipate market shifts, allowing for timely adjustments to your strategy.

- Plan Long-Term: Inflation is a slow and steady force that erodes the value of money over time. Incorporate realistic inflation assumptions into your long-term financial planning to ensure that your savings and investments retain their purchasing power.

By demystifying inflation, you empower yourself to navigate market turbulence with confidence. Knowledge of how and why inflation works is not just academic, it’s a tool for smarter investing.

Conclusion: Transforming Knowledge into Strategy

At its core, inflation is about balance, between money and goods, stability and growth, caution and opportunity. Historical lessons remind us that both extreme scarcity and excessive abundance of money have their dangers. For investors and everyday citizens alike, understanding these dynamics helps transform confusion into clarity. When you grasp the simple math behind inflation, you learn to cut through economic noise and build strategies that not only preserve but also grow your wealth over time.

Reference Links:

- Federal Reserve (federalreserve.gov)

- Fisher Investments (fisherinvestments.com)

- Aier.org (aier.org)

- St. Louis Fed (stlouisfed.org)

- Politico (politico.com)

- Brookings (brookings.edu)

- EconLib (econlib.org)

By drawing from a range of public domain insights and real-world examples, this post aims to make complex economic ideas accessible, enabling you to learn from past mistakes and apply these lessons to your financial journey.